During the past eight-year bull market in US equities, investors have not only reaped the rewards of double-digit compounded returns but have also been able to keep more of those returns for themselves as fund management fees have plummeted. The shift in assets way from actively managed mutual funds toward passively managed (index) funds, along with the proliferation of low-cost exchange-traded funds (ETFs) has created an upheaval in the investment marketplace as fund managers of all stripes have been forced to re-assess and lower the fees they charge for their services. This trend has been bolstered by academic studies quantifying the benefits of passive indexing strategies, as well as by a growing chorus of investment gurus, including the likes of Warren Buffett, who have sung the praises of passive investing as a core strategy for most individual investors. Aside from the lower cost, systematically investing in passive investment vehicles has also proven to somewhat suppress the return-chasing and other behavioral mistakes that investors tend to inflict upon themselves.

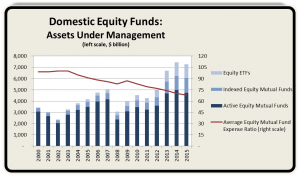

In the US domestic equity segment of the mutual fund marketplace, the share of actively managed funds has dropped from 89% in 2000 to 65% as of the end of 2015. Furthermore, a large portion of the active funds that remain (estimated to be >10% by assets) is comprised of what the industry considers ‘closet indexers’ – funds where a high percentage of their holdings simply replicate the underlying benchmark index against which their returns are compared. This means that the holdings of truly active equity investment managers now comprise only slightly over half of the domestic equity fund market. The long-term implications of this tectonic shift are only now starting to be widely assessed.

Source: ICI

Like most things that seem too good to be true, when one looks below the surface and begins to examine some of the direct and indirect implications of this massive redirection of capital, some inefficiencies and contradictions arise that lead serious investors to whisper concerns about an over correction. These concerns boil down to five arguments:

- Passive investing is an abrogation of duty on the part of the investor – Start by going back to the basic foundation of finance. Fundamentally, financial markets exist to intelligently allocate capital to where it will be used most efficiently, productively, and profitably. This necessitates a value judgment on the part of the decision-making investor. Passive investing, conversely, relieves the investor of his or her obligation to make such a judgment, as assets are allocated across all components within each desired asset class or index on a pro rata basis according to the weightings that the rest of the market, not the investor himself, has previously established. Criticism of this ‘value-blind’ allocation strategy ranges from those who view it as creating a new sort of market ‘bubble’ to those who believe it is antithetical to capitalist principles.

- Almost all passive strategies have some active component to them – An investor who passively invests in an S&P 500 Index ETF is, in fact, making a value judgement – ie, that equities meeting qualification for inclusion in the index are better investments than those excluded from the index. As more and more investors make this determination, as has in fact been the case as funds have disproportionately flowed into these major index ETFs, those favored asset classes and sectors will inevitably become overvalued relative to their less-beloved counterparts.

- The recent success of passive strategies must be viewed in light of unsustainable trends which are partially responsible for that success – When funds flow into passive ETFs, the prices of the underlying holdings of those ETFs will be bid up. Since we have seen nothing but inflows into these strategies over the course of several years, by necessity the lucrative returns enjoyed by almost all such strategies have been attributable to this self-fulfilling prophecy. It remains to be seen whether a reversal of fund flows might have a similar outsized impact on the way back down. The sample size is too small for now to provide sufficient evidence to predict ETF investor behavior in a significant and prolonged market downturn.

- Passive ownership by a few large institutions creates perverse incentives for the underlying corporations they hold –The Big Three ETF providers (BlackRock, Vanguard, and State Street) taken together would represent the largest investor in 88% of S&P500 companies. Since the Big Three are not able to exercise any discretion over allocating funds among their holdings, they have limited ability to hold the management teams at those companies to account. What’s more, since the passive institutional holdings at one company are likely to be replicated at most, if not all, of its competitors, there is no incentive for those institutions to coax the management teams at any one of those companies to compete too aggressively against their peers. Since they have a large stake in ensuring that all underlying holdings perform well in aggregate, they may very well use the influence they do have to encourage a more cooperative posture so as to ensure the viability of all legacy firms in an industry even though a more assertive strategy may be most advantageous to that firm in isolation. Society, therefore, loses out on the benefits of creative destruction. Studies in several industries have shown that product pricing, executive compensation structure, and other corporate strategies become more complacent as common ownership percentages in those industries increase. Furthermore, still other studies have shown that passive investment managers vote in favor of management proposals a significantly greater percentage of the time than do active managers.

- Changing economic and competitive conditions impact different sectors and different companies differently, but passive investing blurs the distinctions – Passive investing tends to increase the price correlations between assets as funds flow en masse to and from large blocs of investments with similar, but not identical, characteristics. Therefore, the impact from changing conditions tends to be over-emphasized in the stock performance of companies which should not be affected by them and under-emphasized in the prices of those companies on which they should have the greatest impact.

What To Do

Despite these criticisms, the evidence in favor of using passive vehicles as the basis for most investment strategies is overwhelming. There are, however, some steps investors can take to intelligently address some of the contradictions in those strategies.

- Employ actively managed funds in sectors prone to inefficiency . . .

According to Morningstar, from 1992 to 2015 actively managed US Large Cap mutual funds underperformed their passive counterparts by 0.71 percentage points. For US Small Cap funds, however, active outperformed passive by 0.99 percentage points; and for International Large Cap, the outperformance was 0.85 percentage points.

- . . . but carefully select those active managers . . .

By limiting one’s selection of actively managed funds across all categories to the lowest expense quartile and sticking to 1 of 5 largest fund families (Fidelity, Vanguard, American Funds, Franklin Templeton, and T. Rowe Price), one would have outperformed the underlying indexes by 0.18 percentage points from 1992 to 2015. As a bigger percentage of the market becomes blindly passive, the ability of remaining active managers to exploit inefficiencies and mispricing becomes greater.

- . . . and avoid closet indexers.

Pay attention to the underlying holdings of active managers also. If a fund’s holdings are large and its index tracking error is low, you may be paying active (high) expenses for passive (average) returns. In that case, stick with index funds and ETFs instead.

- Should volatility return to the market, exploitable opportunities for active managers will increase.

And due to the fact that a higher percentage of investors are passive than ever before, the competition for seizing those opportunities will be less, making actively managed funds and platforms all the more attractive.

- Watch for companies within beaten-down sectors.

When investors sell out of certain industry ETFs, as we have recently seen with banking and healthcare, the catalyst for the selloff is certain to impact different companies within that particular industry to different degrees. The broad-brush impact of major market movements in sector ETFs creates opportunities for finding value in individual stocks.

- Remain disciplined.

Do not react to short-term phenomena or deviate from a plan which you have created which is based on successful, long-term strategies. A study by Dalbar has shown that passive strategies outperform in rising markets but underperform in falling ones. That can only be true if investors alter their behavior in times of stress, to their detriment. Remember, just because passive investments are guaranteed to always achieve average results does not mean that passive investors will do the same, if they lack the discipline to ride out the tough times.

- Consult an advisor.

An advisor can assist in reassuring you about your strategy and help you maintain the aforementioned discipline, not to mention crafting a customized plan that addresses your unique tax, risk, and cash flow needs and goals.

The next significant market downturn will occur sooner or, preferably, later. And only when it does, can we make a true and complete cost/benefit assessment of the impact that the trend toward passive investing has had on the financial lives of US investors as a whole.

By Kevin Fruechte, CFA, Chief Research & Operations Officer of Olson Wealth Group

Copyright. Olson Wealth Group, Minneapolis, Minnesota

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.