Investors that hold a large portion of their net worth in a single stock can be at risk for a number of reasons. Let’s talk about when to hold and when to diversify.

Concentrated stock can be accumulated in a number of ways. Senior executives receive company stock as a major part of their compensation, business owners can receive stock when they sell their company, and inherited single stock portfolios are common in family trusts. The reasons for holding a disproportionate amount of a single stock can be varied from insider selling constraints to emotional attachment to the tax implications of selling. However, studies show that concentrated stock (10% or more of one’s portfolio) can present hidden risks that should be understood and managed.

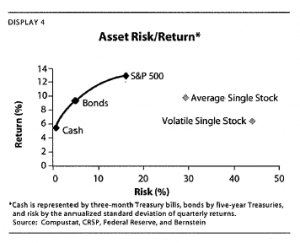

One misconception that many investors have is that an individual stock will provide outsized returns, however, the data below suggests otherwise. Over the last 20 years, individual stocks with average volatility have lagged S&P 500 returns by nearly three percentage points per year while highly volatile stock returns are close to seven points lower. Both have generated bond-like returns (or worse) with much higher volatility than the S&P 500. In short, volatility eats away at returns over the long-run.

Aside from the risk of under performing the broader market, a concentrated stock has the potential to destroy wealth and prevent attainment of basic goals: retirement, college tuition, etc. In addition, returns become too reliant on the fortunes of one company or a single industry. Innovation is great for humanity but can and will eliminate companies and even entire industries over time. Employees holding stock in their company may lose both their source of income (paycheck) and wealth (stock value) as the company fails or the industry suffers a downturn.

To sell or not to sell.

In each case, the variables are unique. For example, a 75-year-old investor who expects to bequeath their assets in the near term might not want to sell at all. A trusted financial advisor will consider risk profile, the investor’s age, investment time horizon, annual spending needs, and the percent of net worth in a single stock position. They can weigh stock volatility, long term growth, and tax implications against the investor’s time horizon and investment goals to develop an appropriate strategy.

Options to reduce the pain and increase the gain.

Diversifying a concentrated position needs to be well thought out and carefully planned. Selling the stock in a single transaction may be the fastest way to reduce volatility and risk but the upfront tax bill might be hard to digest. Also, depending on the size of the stock and transaction, a large sell order can drive down the price of the shares being sold. A staged sale may be considered in this instance.

With a staged sale, investors set a goal of selling a certain number of shares by certain dates and/or share prices. When an investor makes this commitment, they are less likely to be swayed by emotion and market fluctuation. In other cases, executives may be prevented due to insider information and regulatory scrutiny. Staged selling through a 10b5-1 plan might work to remove the investor from the transaction and complete the execution automatically.

Exchange funds offer investors the ability to make a tax-free exchange of an individual stock position into a diversified portfolio. While the investor maintains their original basis in the investment they have eliminated the single stock risk and may be more comfortable holding the more diversified portfolio and postponing any taxable sales. And for the philanthropically minded, a charitable remainder trust (CRT) might work for investors with longer time horizons and appropriate liquidity.

Please call us at any time if you have questions about concentrated risk and the options available to you. At Olson Wealth Group, we understand that wealth comes with great opportunity, responsibility and complexity. You control the destination and purpose of your wealth. We steward that wealth management process with wise choices and clear strategies.

By Michael D. Kotila, CFP® and President of Financial Planning at Olson Wealth Group.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Stock investing involves risk including loss of principal. This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.